The same principles the wealthiest organizations have used for decades, structured for retired and near-retirement families who want to keep more of what they've built.

The Strategy for Protecting Your Wealth

When it comes to securing your financial future, the focus isn't just on how much money you make; it's on how much you keep. In today's volatile financial landscape, safeguarding your wealth from market losses, fees, and unexpected downturns is critical. That's where capital preservation comes in: a proven strategy that protects your hard-earned money from two of the three leaks I see draining most retirement savings (market risk and management fees), while still allowing it to grow steadily over time.

What Is Capital Preservation?

Capital preservation is a savings-focused approach designed to protect your principal from market losses. Unlike traditional investment vehicles that carry inherent risks, capital preservation uses indexed-based strategies that mirror the market's performance without participating in its losses. The cornerstone of this strategy is the floor of zero, which keeps your savings intact even during market downturns. Any gains you achieve are locked in, creating a new, secure baseline for your wealth moving forward.

Why You Haven't Heard of This

Some may question how a strategy like this can protect your money. The answer is straightforward: indexed-based strategies have been around for over 25 years and are backed by reliable financial instruments. As a specialist, I focus ONLY on strategies that minimize risk and fees from your portfolio and, by doing so, help you conserve more of your capital.

These aren't fringe instruments. Banks, corporations, and wealthy families have used capital preservation strategies for decades to protect their assets from the same forces that quietly put household retirement accounts at risk. The reason most retirement savers haven't encountered them isn't that they don't work; it's that they sit on the protection side of the financial industry, separate from the growth-focused vehicles most retirement accounts are built on. My role is to introduce you to an approach many families wish they had discovered sooner.

A Decade Under Two Rules

Same market. Same start. Two very different endings.

S&P 500 (market)Indexed · 0% floor · 10% cap

Illustrative. Based on S&P 500 annual index changes 2000–2010 (excluding dividends, as indexed products use). Indexed line assumes a 10% annual cap, 100% participation, and 0% floor. Actual product terms vary — this is a mechanic, not a projection.

Key Features of Capital Preservation

Minimal Risk, Built-In Stability. Capital preservation ensures your principal is protected from market loss. Gains are locked in, and losses are avoided thanks to the floor of zero. This creates peace of mind, since you know your wealth is protected.

Growth Without Losses. Any market gains are mirrored and added to your savings, but you do not participate in market losses. Once a gain is locked in, it becomes your new baseline, providing security while still allowing for steady growth.

Zero Management Fees. One of the most significant advantages of capital preservation is that it doesn't come with management fees. Traditional strategies often charge a percentage of your account annually, typically 1 to 3 percent on average, REGARDLESS if your account grows or loses, which can significantly reduce your savings over time.

For example, a $500,000 account would lose $5,000 to $15,000 a year in fees under a typical plan. With capital preservation, there are no management fees, so every dollar you save stays in your account, helping you reach your financial goals faster and more efficiently.

How It Works

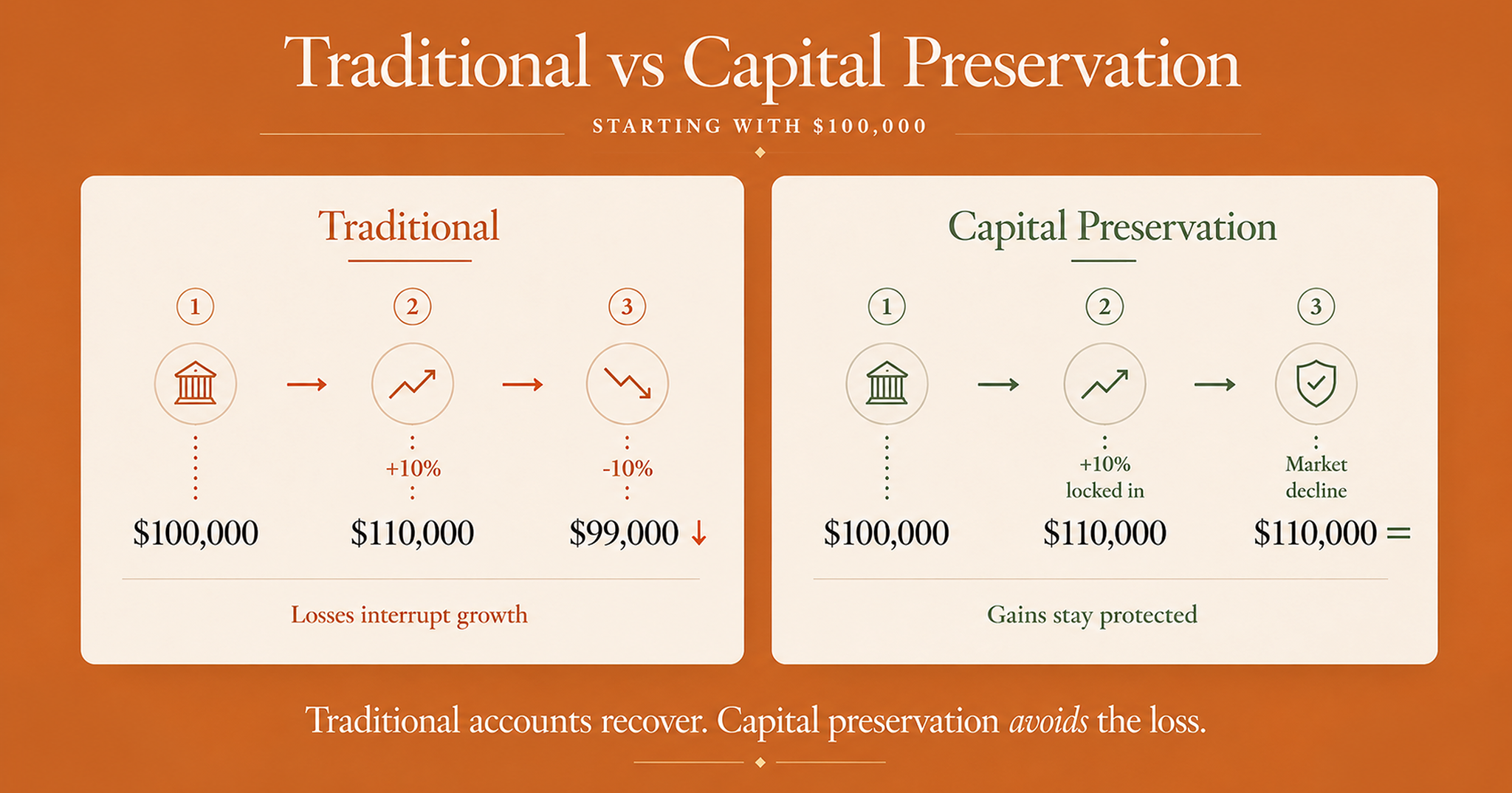

Imagine starting with $100,000. In a traditional investment scenario, a 10 percent market gain might be followed by a 10 percent loss, leaving you below where you started. With capital preservation, that same 10 percent gain is locked in, and any market decline doesn't affect your savings. This is the power of uninterrupted compounding: where a traditional account spends years recovering from each downturn, capital preservation doesn't take those losses in the first place, so every gain builds on the one before it.

Implementing Capital Preservation: A Step-by-Step Approach

Assess Your Goals. I start by asking how important it is to you to eliminate risks and fees from your current financial strategy. If the answer is high on the priority list, it's time to evaluate where your money is currently parked.

Decide Between Risk and Security. Many of my clients face a choice: continue with a strategy that exposes their wealth to market volatility and fees, or reposition into an indexed-based approach that allows for steady growth without the loss. For those who prioritize stability and long-term security, the decision is clear.

Work with a Specialist. My goal is to create a tailored plan that fits your unique situation. The aim is to ensure your savings are not only protected but positioned for modest, consistent growth that aligns with your financial goals.

It's Not About Making Money. It's About Keeping It.

In retirement, the focus shifts from earning more to preserving what you've built. By eliminating risk and fees, you avoid the lost opportunity of market downturns and create a foundation for steady growth. This isn't just a strategy. It's a mindset.

— Let's Talk

Ready to see if capital preservation fits your situation?

Book a 10-minute call. I'll look at where your money is currently parked, listen to what you're trying to protect, and tell you honestly whether this is the right move.

Most retirement savings in this country sit inside tax-deferred accounts: 401(k)s, IRAs, 403(b)s, 457(b)s, SEP IRAs. These accounts have become the default, and most people assume they were designed for retirement. They weren't. They're tax-deferred instruments, which means the government postpones the bill on what you earn; it doesn't remove it. The same money you spent decades building gets taxed on the way out, at whatever the tax code looks like at the time.

There's another side to retirement planning that most people are never introduced to. It's called the tax-free side, and it's where I do most of my work.

The Truth About Tax-Deferred Accounts

When most people picture their 401(k) or IRA, they picture a retirement account. What it actually is, mechanically, is a tax-deferred holding account exposed to the market. The structure carries seven realities that aren't well understood:

You're taxed at the time you typically need the money the most.

You generally cannot touch your money until age 59½ without penalty.

Your account is subject to market risk and volatility. When the market drops, your account drops with it.

There's no certainty about how much money will be left when it's time to access it.

Restrictions and penalties limit access to your own money before retirement age.

Every dollar you withdraw is reported as taxable income to the IRS.

The IRS has a permanent claim on the account, regardless of what you earn or withdraw.

Put simply: the account in your name isn't entirely yours. A portion of it belongs to the IRS, and they decide when to collect.

Graduating to the Tax-Free Side

A properly structured tax-free strategy is a different instrument entirely. When designed and structured correctly under IRS guidelines, it offers six features the tax-deferred side cannot:

You don't pay taxes on your principal or your growth.

You typically keep 30 to 40 percent more of your money than you would on a tax-deferred path.

Principal protection is built in, without sacrificing growth.

Your money compounds without interruption, year after year.

Your money stays liquid and accessible at any time, without penalties or restrictions.

When structured correctly, accessing your money is not classified as taxable income, so it doesn't add to your taxable income, whether you take out $10,000 or $500,000.

The result is a retirement account that grows tax-free, is structured for tax-free access, and stays in your control from the day you open it.

Why Most People Haven't Heard of This

There's a simple reason most retirement savers haven't been introduced to tax-free strategies: the tax-free side of finance sits in a different lane than the tax-deferred side, and the two require different licensing, training, and specialization.

The tax-deferred side is heavily standardized. The accounts are largely identical, the rules are uniform, and the path most people are walked through, whether by HR at their job or an advisor at a firm, is a near-identical plan. It scales because it doesn't require much personalization.

The tax-free side works differently. There are no cookie-cutter scenarios; every plan requires real consultation, real personalization, and a working knowledge of how the structures fit together. That's the work I specialize in, and it's why most of my conversations start with someone who's been saving diligently for decades and has simply never been shown the other half of the picture.

What This Strategy Plugs

On the About page, I describe the three leaks that quietly drain most retirement savings: risk, fees, and taxes. Capital preservation strategies address the first two. A properly structured tax-free strategy is built to plug the third.

The implication is significant. Taxes are the leak most people don't realize they're carrying, because the bill doesn't show up in any given year; it shows up at retirement, when you begin accessing your money. By that point, the rate has already been set by whatever the tax code looks like at the time, and the saver has no leverage to do anything about it.

A tax-free strategy moves that decision out of the IRS's hands and back into yours.

A Question Worth Sitting With

How much money are you willing to lose in your 401(k) or IRA — to taxes, to a market downturn, to fees compounding silently against you?

If the honest answer is ‘nothing’, then what you want isn't matching what you currently have. That's the conversation worth having.

Here's the truth: retirement tax rates are near historic lows right now. With the national debt in the headlines almost daily, the pressure only runs one direction — toward higher rates, or the sneakier move, expanding what counts as taxable without ever touching the rate. A tax-deferred account is a bet that the rules won't change against you between now and the day you retire.

Time matters in retirement planning, and being uninformed about your own money is the most expensive position to hold. The strategies that plug the tax leak exist; they've existed for decades. Whether they're a fit for your situation is what a short conversation can tell us.

— Let's Talk

Ready to see if a tax-free strategy fits your situation?

Book a 10-minute call. I'll look at where your money is currently parked, walk you through what a tax-free strategy would look like for your specific picture, and tell you honestly whether it's the right move.